04,24,2026 238 views

【instrumentInternet industry data】Chromatography and mass spectrometry instruments, as core equipment in the field of inspection and testing, are widely used in key areas such as food safety, public health, drug inspection, and environmental monitoring. Their bidding and procurement data directly reflect the industry's demand trends and market patterns. Instrument Network is based on the national bidding and procurement data of chromatography and mass spectrometry instruments from January to March 2026 (Q1), combined with the industry development background, to deeply analyze the procurement characteristics, brand pattern, and future trends, providing reference for industry practitioners, suppliers, and purchasers.

Overall overview of Q1 procurement: Stable scale, with customs as the core driving force

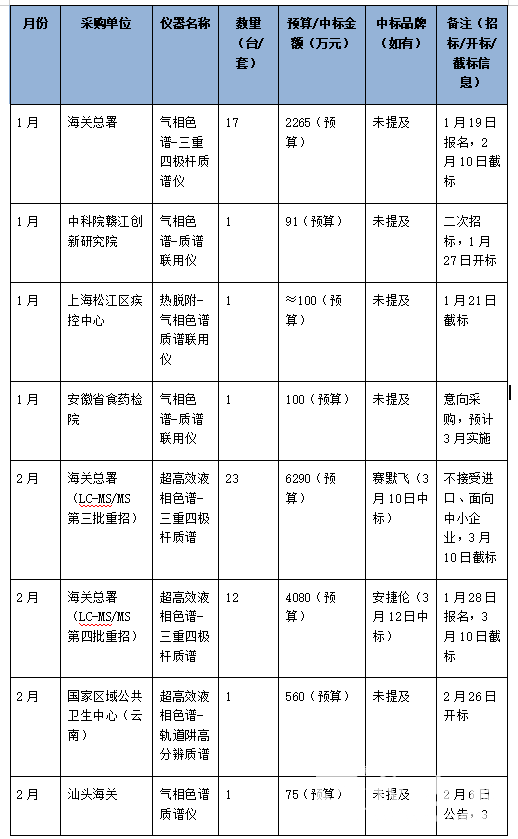

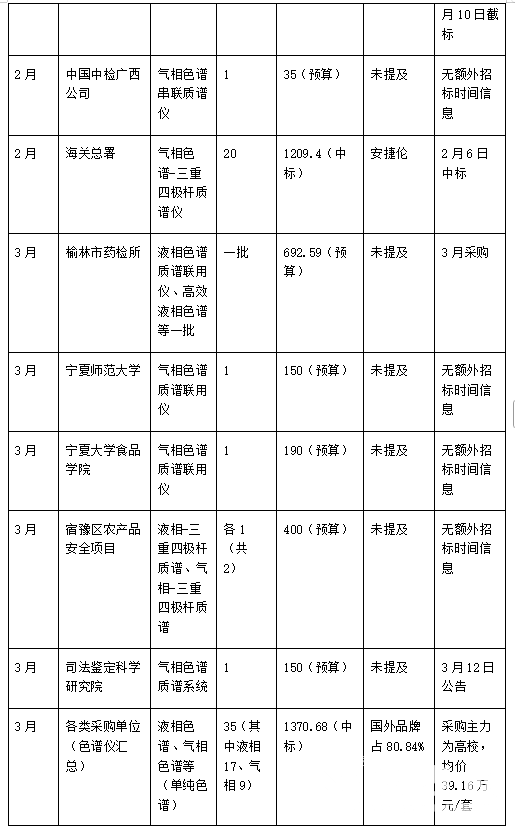

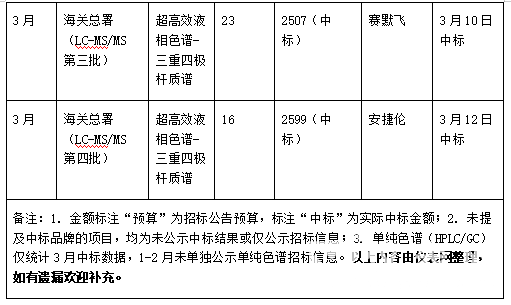

In Q1 of 2026, the total budget for the bidding and procurement of chromatography and mass spectrometry instruments in China exceeded 175 million yuan, and the procurement activities showed the characteristics of "concentrated outbreak and layered promotion". From the distribution within the quarter, January is the start-up period, with a procurement budget of approximately 25.56 million yuan, mainly for single unit/small batch purchases at the million level; In February, we entered the peak of procurement with a total budget of 110.5 million yuan, driven by the bulk procurement projects of the General Administration of Customs; In March, it returned to stability with a budget of about 15.8259 million yuan, and the purchasing entities shifted to universities, local drug testing and agricultural product testing institutions.

From the perspective of procurement entities, the customs system has become the absolute core, with a procurement budget of approximately 126.35 million yuan in Q1, accounting for over 72% of the total quarterly budget, mainly focusing onliquid chromatography-Triple quadrupole mass spectrometry (LC-MS/MS)gas chromatography-Batch procurement of triple quadrupole mass spectrometer (GC-MS/MS); Next are universities and research institutes, with a procurement budget of approximately 11.21 million yuan, mainly for the purchase of single gas chromatography-mass spectrometry (GC-MS) instruments; The procurement budget for drug testing, disease control, and agricultural product testing is approximately 9.4259 million yuan, taking into account both chromatography, mass spectrometry, and simple chromatography instruments to meet daily testing needs.

Core procurement features: model focus, significant differentiation in application scenarios

(1) High concentration of models and mainstream use of combined instruments

The procurement of Q1 models presents a pattern of "combination oriented, simple auxiliary", among which liquid chromatography triple quadrupole mass spectrometry (LC-MS/MS) has become a hot spot for procurement, with a budget of 103.7 million yuan, accounting for nearly 60% of the total quarterly budget, mainly used for large-scale testing needs in the customs system; The gas chromatography-mass spectrometry (GC-MS/GC-MS/MS) has a budget of approximately 37 million yuan and is widely used in university research, disease control testing, and customs special testing; As a high-end model, only one set of ultra-high performance liquid chromatography orbital trap high-resolution mass spectrometry was purchased by the National Regional Public Health Center (Yunnan) with a budget of 5.6 million yuan, reflecting the precise demand for high-end detection equipment.

The HPLC/GC instrument only had clear bidding data in March, with a total of 35 sets winning bids at a price of 13.7068 million yuan and an average price of 391600 yuan per set, including 17 sets of liquid chromatography (7.7817 million yuan) and 9 sets of gas chromatography (3.1512 million yuan), mainly serving basic experiments in universities and routine testing in local testing institutions, with relatively stable demand.

(2) Segmented application scenarios with prominent requirements in core areas

The procurement demand for Q1 mainly focuses on four core scenarios, showing obvious differentiation characteristics: firstly, in the field of customs inspection, it focuses on precise detection of import and export goods and food. The procurement models are mainly LC-MS/MS and GC-MS/MS with high sensitivity and high batch processing capacity. For example, the two batches of LC-MS/MS procurement launched by the Customs General Administration in February, totaling 35 units, with a budget exceeding 103 million yuan, and it is explicitly required to target small and medium-sized enterprises, not accept imports, and comply with national industrial support policies; Secondly, in the field of public health and disease control, represented by the Shanghai Songjiang District Center for Disease Control and Prevention and the National Regional Public Health Center (Yunnan), thermal desorption gas chromatography-mass spectrometry, high-resolution mass spectrometry, etc. are purchased for infectious disease prevention and control, and public health emergency detection; Thirdly, in the field of drug and agricultural product testing, the Yulin Drug Inspection Institute and the Suyu District Agricultural Product Safety Project purchase liquid-phase and gas-phase instruments to ensure the quality and safety of drugs and agricultural products; Fourthly, in the field of scientific research in universities, Ningxia Normal University and the School of Food Science at Ningxia University purchase GC-MS for basic research in disciplines such as food science and environmental science.

(3) Clear price range, highlighting the cost-effectiveness of bulk procurement

From the perspective of purchasing prices, there is a clear stratification in the price range of different models: the price of a single GC-MS is concentrated between 750000 and 1.9 million yuan, such as the GC-MS budget of 1.9 million yuan purchased by the School of Food Science at Ningxia University and 750000 yuan purchased by Shantou Customs; The price of a single LC-MS/MS is concentrated between 2 million and 3.5 million yuan, and the average price for bulk procurement by customs is even lower. For example, the winning bid for the third batch of 23 LC-MS/MS by the General Administration of Customs was 25.07 million yuan, with an average price of about 1.09 million yuan per unit; The price of high-resolution mass spectrometry is over 5 million yuan, which is a scarce demand for high-end equipment. This price distribution is basically consistent with the industry average price level in 2024, with higher average unit prices in regions such as Hainan and Beijing, while relatively lower unit prices in regions such as Ningxia, reflecting regional demand differences.

Brand pattern: Import dominates the high-end market, domestic production welcomes breakthrough opportunities

The procurement market for chromatography and mass spectrometry instruments in Q1 presents a pattern of "import led, domestic breakthrough", which is consistent with the high concentration of industry brands in 2024. From the perspective of winning bids, imported brands have an absolute advantage, with Agilent and Thermo Fisher being the biggest winners: Agilent won the bid for 20 GC-MS (valued at 12.094 million yuan) and 16 LC-MS/MS (valued at 25.99 million yuan) from the General Administration of Customs, with a total bid amount exceeding 38 million yuan; Thermo Fisher has won the bid for 23 LC-MS/MS machines from the General Administration of Customs (with a value of 25.07 million yuan), and the two major brands have taken on the core bulk procurement project for the customs system. Combining industry data, Agilent, Shimadzu, and Thermo Fisher's total market share of gas chromatographs in 2024 reached 77%, with Agilent accounting for 39.88%, Shimadzu 30.26%, and Thermo Fisher 7.31%. The Q1 procurement data further confirms the dominant position of imported brands in the high-end combination instrument field.

It is worth noting that domestic instruments have ushered in an important breakthrough opportunity: the General Administration of Customs launched the third batch of re recruitment for LC-MS/MS in February, which clearly requires "not accepting imports and targeting small and medium-sized enterprises". This policy orientation has opened up market space for domestic instruments. For a long time, imported brands have dominated the large procurement market with their technological advantages, stability, and comprehensive after-sales service, while domestic brands are mainly concentrated in the small and medium-sized, mid to low end model market. According to the bidding data of simple chromatography in March, foreign brands accounted for 80.84% of the total amount, and there is still significant room for improvement in domestic products. However, the policy of special procurement by customs will promote technological breakthroughs and market penetration of domestic instruments in the field of combined instruments. In addition, there are differences in brand preferences among different regions, such as Jiangsu's preference for Shimadzu and Agilent, and Sichuan's preference for Agilent, Shimadzu, and Thermo Fisher. This also provides a reference direction for the regional promotion of domestic instruments.

Industry Trend Insights and Future Prospects

(1) Policy orientation promotes industry upgrading and accelerates domestic substitution

From the Q1 procurement data, the guiding role of policy factors on procurement demand is becoming increasingly prominent. The requirement of "not accepting imports and targeting small and medium-sized enterprises" in the special procurement of the General Administration of Customs, as well as the guidance of "supporting small and medium-sized enterprises and promoting the development of domestic equipment" in government procurement policies, will continue to promote the technological research and market application of domestic chromatography and mass spectrometry instruments. In the future, with the improvement of core indicators such as sensitivity and stability of domestic instruments, it is expected to gradually break the monopoly pattern of imported brands and achieve a wider range of substitution in fields such as customs and local testing institutions. At the same time, local customs procurement projects such as Shantou Customs strictly implement government procurement policies, further expanding the market opportunities for domestic instruments.

(2) Demand focuses on high-end and mass production, with technological iteration becoming the key

According to Q1 procurement data, LC-MS/MS、 The demand for high-end combined instruments such as high-resolution mass spectrometry is strong, and bulk procurement by customs has become the norm, reflecting the industry's increasing demand for precise detection and efficient processing capabilities. In the future, with the continuous improvement of testing standards in fields such as food safety, environmental monitoring, and public health, the demand for high-end chromatography and mass spectrometry instruments will continue to grow. The intelligence, automation, and integration of instruments will become the core direction of technological iteration. At the same time, the demand for high-end instruments from universities and research institutes will gradually increase, promoting the deep integration of scientific research and industry.

(3) Diversified procurement entities and balanced regional demand

The procurement entities of Q1 have extended from traditional customs and universities to local drug testing, disease control, agricultural product testing institutions, and judicial appraisal institutions, and the procurement demand is showing a diversified trend. From a regional perspective, except for developed coastal areas, the procurement demand in central and western regions such as Ningxia, Shaanxi, and Yunnan is gradually being released. Procurement projects such as Ningxia Normal University and Yulin Drug Control Institute reflect the need to improve regional testing capabilities. Based on the 2024 regional bidding data, provinces such as Jiangsu, Sichuan, and Guangdong have a higher proportion of bidding amounts. In the future, with the improvement of public health and food safety testing capabilities in the central and western regions, regional procurement demand will be more balanced.

(4) Brand competition intensifies, and service capability becomes the core competitiveness

At present, there is a high concentration of brands in the chromatography and mass spectrometry instrument market, with imported brands such as Agilent and Thermo Fisher dominating with technological advantages, while domestic instrument companies are accelerating their breakthrough under policy support. In the future, brand competition will shift from simple technical competition to comprehensive competition in terms of technology, price, and after-sales service. For suppliers, it is necessary to focus on the technological research and development of core models, improve instrument stability and detection accuracy, and optimize the after-sales service system to meet the long-term usage needs of buyers; For the purchaser, they will pay more attention to the cost-effectiveness, after-sales service, and localized technical support of the instruments, promoting the healthy development of market competition.

Conclusion

The bidding and procurement market for chromatography and mass spectrometry instruments in Q1 2026 presents the characteristics of "stable scale, optimized structure, and clear policy orientation". Customs bulk procurement dominates the market, and there is a strong demand for high-end combined instruments. Domestic instruments have ushered in important breakthrough opportunities. With the increasing policy support, continuous technological iteration, and diversified procurement needs, the chromatography and mass spectrometry instrument industry will enter a stage of high-quality development.

In the future, domestic instrument companies need to seize policy opportunities, focus on technological innovation, and enhance their core competitiveness; Suppliers need to accurately grasp procurement needs and optimize products and services; The purchaser needs to combine their own needs to achieve an organic combination of equipment procurement and testing capability improvement, and jointly promote the sustainable development of China's precision testing field.