04,24,2026 220 views

【instrumentDepth of the Internet Industry】Electronicmeasuring instrumentAs an "industrial thermometer" for scientific researchmicroscope”It is the core support for the development of the electronic information industry and high-end manufacturing industry, directly related to China's independent and controllable science and technology and industrial upgrading process. The Instrument Network has compiled the 2025 financial report data of six domestic electronic measuring instrument enterprises, namely Dingyang Technology, Puyuan Jingdian, Huashengchang, Chuangyuan Xinke, Youlide, and Tonghui Electronics. Combining industry policies and market environment, it systematically analyzes the current development status, core characteristics, future trends, and challenges of China's electronic measuring instrument industry, providing reference for industry development and enterprise layout.

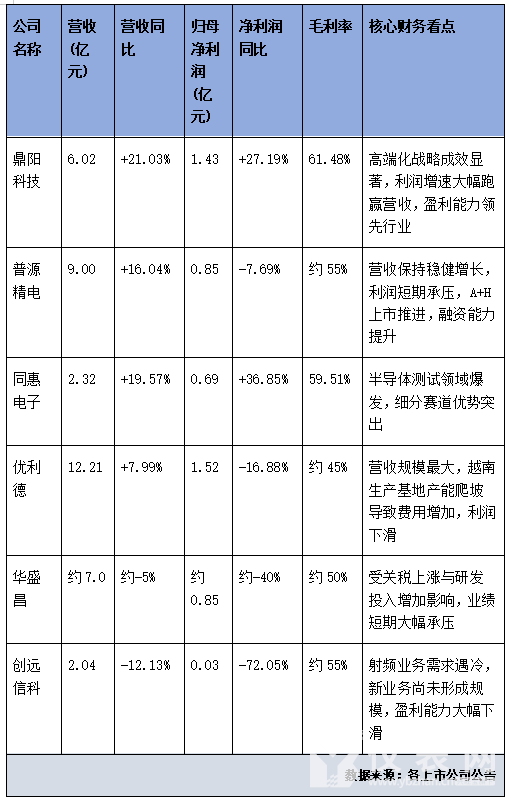

Overview of Financial Data of Six Core Enterprises in 2025

The six selected enterprises cover core sub sectors such as general electronic measurement, high-end RF testing, and semiconductor testing. Their 2025 financial data intuitively reflects the overall development trend of the industry and individual differences among enterprises, as shown in the following table:

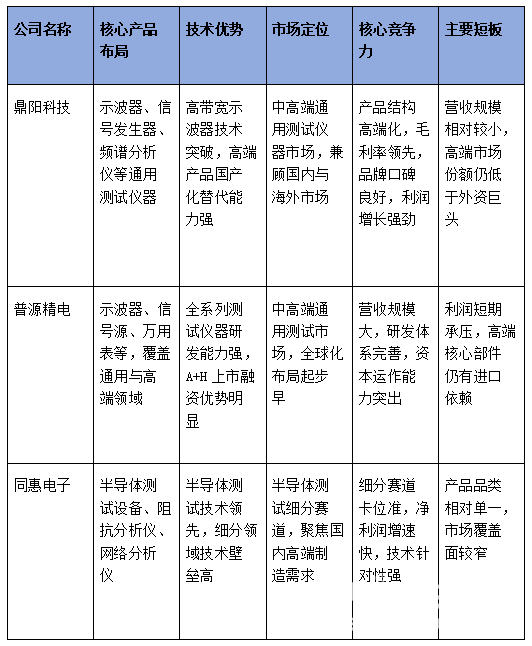

Comparison of Core Competitiveness among Six Companies

There are significant differences among the six companies in terms of product layout, technological advantages, market positioning, and core weaknesses, forming their own competitive barriers. The specific comparison is as follows:

Core Characteristics of the Development of China's Electronic Measuring Instrument Industry as Reflected in Financial Reports

(1) The industry as a whole maintains growth, and domestic substitution enters the deep-water zone

From the overall performance of the six companies, the total revenue in 2025 is about 3.86 billion yuan, maintaining a medium to high growth trend. Among them, Dingyang Technology and Tonghui Electronics both have revenue growth rates exceeding 19%, significantly higher than the global average growth rate of 0% -8% in the electronic measuring instrument industry, demonstrating the strong growth momentum of domestic manufacturers. Behind this growth trend, strong policy support is indispensable: the "Metrology Development Plan (2025-2035)" explicitly states that "the government procurement ratio of domestically produced measuring instruments shall not be less than 50%" and pilot the "domestication rate" veto system, directly opening up a vast domestic market space for domestic manufacturers.

In terms of market size, the market size of electronic measuring instruments in China has exceeded 40 billion yuan by 2025 and is expected to exceed 50 billion yuan by 2030, with a compound annual growth rate of 8% -10%. With the continuous upgrading of downstream industries such as electronic information, high-end manufacturing, and new energy in China, the market demand for domestic electronic measuring instruments will be further released, and domestic substitution will move from "low-end substitution" to "high-end substitution" and enter a stage of deep development.

(2) High end industry winners and losers, gradually breaking through technological barriers

According to financial report data, companies that focus on high-end layout have shown more outstanding performance: Dingyang Technology has increased its proportion of high-end oscilloscopes and other products, with a gross profit margin of 61.48% and a net profit growth rate of 27.19%, significantly exceeding the revenue growth rate of 21.03%; Tonghui Electronics focuses on the high-end sub segment of semiconductor testing, with a revenue growth rate of 154.88% for its core product TH300 series system integration testing equipment, driving a net profit growth rate of 36.85%, leading six companies.

In terms of breakthroughs in core technologies, domestic electronic measuring instruments have achieved a leap from "GHz level" to "10GHz+". In 2025, a 90GHz ultra high speed real-time oscilloscope will be launched, breaking the technological monopoly and embargo barriers of foreign enterprises in the high-end oscilloscope field. To support technological breakthroughs, all six companies have increased their R&D investment, with R&D expense ratios generally maintained at 10% -15%. Among them, Chuangyuan Xinke focuses on the field of RF communication testing and has launched high-end new products such as 44GHz handheld spectrum analyzers, attempting to break through business bottlenecks.

(3) Industry structural differentiation intensifies, highlighting the Matthew effect

The financial performance of six companies in 2025 shows a clear differentiation trend. One type is the "strong always strong" camp: Dingyang Technology and Tonghui Electronics have achieved dual high growth in revenue and profit through precise high-end positioning and deep cultivation of segmented tracks, with outstanding profitability and becoming leaders in industry development; Another type is the "pressure highlighted" camp: Chuangyuan Xinke and Huashengchang have experienced significant declines in revenue and net profit due to macroeconomic factors, downstream 5G construction slowdown, and tariff increases. Among them, Chuangyuan Xinke's net profit has decreased by 72.05% year-on-year, intensifying survival pressure; In addition, as the company with the largest revenue scale among the six enterprises (1.221 billion yuan), Ulide has experienced an imbalance between scale and profit due to the increase in production capacity and operating expenses of its Vietnam production base, resulting in a year-on-year decline of 16.88% in net profit.

Behind this differentiation, the essence lies in the difference between corporate strategic layout and core competitiveness: companies that focus on high-end and deeply cultivate segmented tracks can withstand industry fluctuations and achieve steady growth; Enterprises that rely on the mid to low end market, have a single business structure, and are greatly influenced by the external environment face greater operational pressure. The intensification of industry competition further compresses the survival space of small and medium-sized manufacturers.

(4) The downstream application drive is obvious, and the emerging track is experiencing explosive growth

The demand for electronic measuring instruments is highly correlated with the development of downstream industries. The 2025 financial report data clearly reflects the structural changes in downstream applications: firstly, semiconductor testing has become a golden track, and the explosive growth of Tonghui Electronics confirms the strong demand for high-end testing instruments in the semiconductor industry. With the improvement of the domestic semiconductor industry chain, the market space for semiconductor testing instruments will continue to expand; Secondly, there is a strong demand in the fields of new energy and communication. Emerging industries such as new energy vehicles, photovoltaics, and 6G communication have seen a surge in demand for high-precision, high bandwidth, and multi-channel electronic measuring instruments, providing sustained growth momentum for the industry; Thirdly, the basic disk of general instruments is stable, and general instruments such as multimeters and oscilloscopes are still the main demand in the market. Domestic manufacturers dominate the mid to low end general instrument market with their high cost-effectiveness advantages, providing stable revenue support for enterprises.

(5) Globalization layout accelerates, opportunities and risks coexist

In order to cope with international trade frictions and optimize supply chain layout, leading domestic enterprises have launched globalization layouts one after another: companies such as Ulide and Huashengchang have built production bases in Vietnam to reduce tariff costs and supply chain risks; Puyuan Jingdian is promoting the listing of A+H, expanding financing channels, and accelerating global market expansion and technology research and development. However, at the same time, globalization has also brought new challenges: the high-end market is still monopolized by foreign giants such as DeTech and Rohde&Schwarz, with a total market share of 40% -50%. Domestic manufacturers still have a gap with the international top level in core areas such as ultra-high frequency and high precision; In addition, fluctuations in trade policies and exchange rates in overseas markets also have a certain impact on a company's overseas revenue.

Development Trends and Core Challenges of China's Electronic Measuring Instrument Industry

(1) Three major development trends for the future

Technology continues to evolve towards "high, precision, and intelligence".With the upgrading of downstream industries towards high-end and intelligent, electronic measuring instruments will gradually develop towards the direction of "high frequency, large bandwidth, multi-channel, intelligence, and software". The deep empowerment of AI technology will become an important trend, achieving automatic analysis and fault diagnosis of test data through AI algorithms, and improving testing efficiency; Modular and virtual instruments will become mainstream, meeting users' personalized and customized testing needs and reducing testing costs.

Domestic substitution is deeply penetrating into high-end fields.At present, the domestic substitution of low-end electronic measuring instruments in the domestic market has been basically completed. In the future, the core of domestic substitution will focus on high-end fields such as 10GHz+oscilloscopes, high-end RF testing instruments, semiconductor testing equipment, etc., which will become the key focus of domestic manufacturers. With the increasing policy support and continuous increase in research and development investment, the localization rate of domestic instruments will continue to improve, gradually breaking the monopoly of foreign giants in the high-end market.

The business model is transitioning from "selling products" to "selling solutions".The business model of selling a single instrument is no longer sufficient to meet the comprehensive testing needs of downstream enterprises. In the future, the industry will gradually transition from a "product oriented" to a "solution oriented" approach. Enterprises will rely on their technological advantages to provide downstream customers with system level testing solutions, covering full chain services such as instrument sales, software services, technical support, and customized development. Software and services will become new profit growth points, enhancing the profitability and customer stickiness of enterprises.

(2) Core challenges faced

There is a gap between high-end technology and core components.Although domestic electronic measuring instruments have achieved some breakthroughs in the mid to high end field, there is still a gap of 1-2 generations compared to the international top level in core indicators such as ultra-high frequency (>110GHz) and ultra-high precision; Key core components such as high-end chips, core algorithms, and precision sensors still rely on imports, which poses a risk of "bottleneck" and restricts the research and industrialization of high-end products.

The bottleneck between talent and funding is prominent.The electronic measuring instrument industry is a technology intensive industry that requires a large number of high-end R&D talents with knowledge in multiple disciplines such as electronic engineering, computer science, and mathematics. However, there is currently a shortage of high-end talents in related fields in China, which has become an important limiting factor for technological breakthroughs; At the same time, sustained high-intensity R&D investment puts significant pressure on the cash flow of enterprises, making it difficult for small and medium-sized manufacturers to bear long-term R&D investment, leading to a trend of "head concentration" in industry technology R&D and insufficient innovation capabilities of small and medium-sized enterprises.

The market competition is intensifying, and profit margins are being compressed.There are numerous domestic manufacturers of electronic measuring instruments, and the competition in the mid to low end market is severe due to homogenization and intense price wars, resulting in generally low gross profit margins for enterprises (such as Youlide's gross profit margin of only about 45%); The high-end market is monopolized by foreign giants, and domestic manufacturers need to invest a large amount of research and development and marketing costs to break through, further compressing profit margins. Some enterprises are trapped in the dilemma of "high research and development investment and low profitability".

Summary and Outlook

2025 is a crucial year for the development of China's electronic measuring instrument industry, and the financial reports of six listed companies jointly confirm the industry's high prosperity driven by policy dividends, technological breakthroughs, and domestic substitution. Among them, leading enterprises such as Dingyang Technology and Tonghui Electronics have achieved dual high growth in revenue and profit through high-end layout and deep cultivation of segmented tracks, leading the industry to transform towards high-end and intelligent development; However, Ulide, Huashengchang, and Chuangyuan Xinke are facing varying degrees of operational pressure, reflecting the reality of structural differentiation in the industry and the challenges faced by domestic manufacturers in the process of globalization layout and technological breakthroughs.

Looking ahead to the future, China's electronic measuring instrument industry will continue to follow the path of "domestic substitution, high-end breakthrough, and intelligent transformation". With the continuous increase in policy support, research and development investment, and downstream demand, domestic electronic measuring instruments are expected to occupy a more important position in the global market and become an important support for the development of China's high-end manufacturing industry. However, at the same time, domestic manufacturers also need to face issues such as the gap in high-end technology and talent and funding bottlenecks. Through technological innovation, business model upgrades, and global layout optimization, they can break through development bottlenecks and promote the high-quality development of China's electronic measuring instrument industry.

Risk Warning: The data in this article is sourced from announcements of listed companies. There are risks in the market, and investments should be made with caution.