04,24,2026 238 views

【instrumentDepth of the Internet Industry】From 2025 to 2026, a competition will revolve aroundinstrumentation and meters、sensorThe wave of Hong Kong stock listings for industrial control and precision testing equipment is underway. From industry leaders that have already been listed, to specialized and innovative enterprises that have submitted reports intensively, and to segmented champions who have launched the "A+H" plan one after another, domestic instruments and meters are accelerating towards high-end and globalization with the help of the Hong Kong capital market.

According to the statistics of Instrumental Network, as of April 2026, there are a total of 10 instrumentation and related enterprises (including automation, sensors, and precision testing) planned or already listed on the Hong Kong Stock Exchange from 2025 to 2026, covering three major stages of listing, submission for trial, and preparation for launch, forming a full tier listing wave.

Triple drive drives Hong Kong stock market listing frenzy

This round of instrument and meter companies going public in Hong Kong is not simply a financing demand, but the result of the resonance of industry cycles, corporate strategies, and capital markets

(1) Domestic substitution enters the 'deep water zone', capital helps break through the situation

The current instrumentation industry is in a critical stage of accelerating domestic substitution and tackling high-end challenges. On the one hand, the industry scale has exceeded one trillion yuan, and the domestic market share of domestic instruments has reached 58%. However, the high-end market is still monopolized by foreign companies such as Thermo Fisher and Agilent, and the dependence on imported core components exceeds 60%. On the other hand, intelligent manufacturing, new energy, semiconductors, and dual carbon targets have generated a massive demand for high-end instruments, with segmented markets such as lithium battery monitoring, carbon monitoring, and industrial visual inspection growing at an annual rate of over 20%.

Listing on the Hong Kong stock market has become an important support for companies to break through technological bottlenecks and seize the high-end market. Fundraising can be used for high-end instrument research and development (such as Puyuan Jingdian focusing on 90GHz high-end oscilloscopes), core chip self-developed, and capacity expansion. At the same time, leveraging the international capital attributes of Hong Kong stocks, it can accelerate the global certification and market expansion of high-end products.

(2) Global expansion accelerates, A+H builds' dual platforms'

This round of listed companies presents three major commonalities: a high proportion of overseas business, strong technological barriers, and urgent international demands. Estun, Junsheng Electronics, Sanhua Intelligent Control and other companies have overseas revenue accounting for over 35%, with products covering more than 90 countries and regions worldwide. However, there are still shortcomings in brand recognition, localized operations, and international capital docking.

The "A+H" dual platform strategy has become the optimal solution: firstly, diversified financing, flexible refinancing mechanism for Hong Kong stocks, with a 30% shorter cycle compared to A-shares, facilitating cross-border mergers and acquisitions and overseas production capacity layout; The second is brand internationalization. Listing on the Hong Kong stock market gives companies the status of "international public companies", enhances global customer trust, and helps break through barriers in overseas markets; The third is to upgrade governance, align with Hong Kong's dual regulatory standards, optimize corporate governance, and attract high-end talents from around the world.

(3) Hong Kong stock policies are favorable, and the valuation of the technology sector is recovering

In 2026, the Hong Kong IPO market experienced a surge, with fundraising reaching HKD 109.927 billion in the first quarter, a year-on-year increase of 489%. Technology and high-end manufacturing became the core tracks. The Hong Kong Stock Exchange's "Science and Technology Enterprise Special Line" (Chapter 18C) has opened a green channel for the review of special technology enterprises, simplifying the recognition of voting rights structure, and directly benefiting enterprises such as Puyuan Jingdian.

At the same time, the valuation of the technology sector in Hong Kong stocks is gradually recovering, with an average price to earnings ratio (TTM) of about 35 times, higher than the average of 28 times in the A-share general equipment industry, providing room for valuation improvement for instrument and meter companies. Combined with the increasing attention of global capital to China's high-end manufacturing, Hong Kong stocks have become the preferred destination for instrument and meter leaders to connect with international capital.

Leading in four major sub sectors, driven by both technology and market

From the layout of listed companies, the industry presents the characteristics of concentrated tracks and prominent advantages, with four major sub sectors becoming capital darlings:

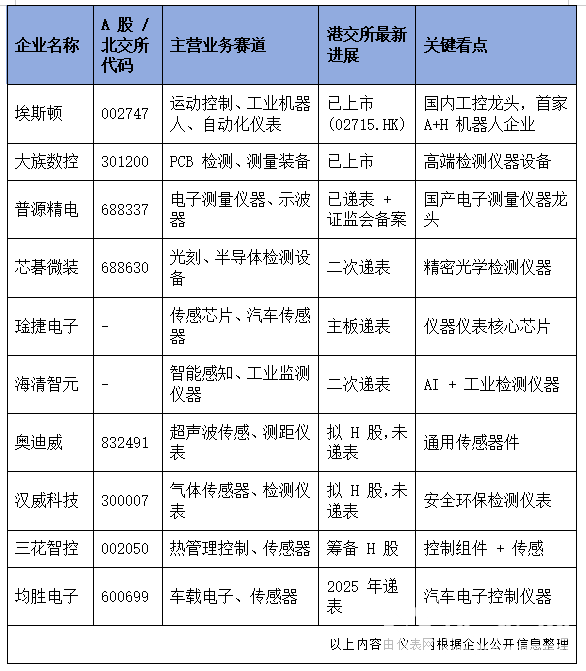

(1) Electronic measuring instruments: domestic replacement of core positions

Represented by Puyuan Precision Electric, it focuses on digital oscilloscopes, spectrum analyzers, and RF microwave instruments, which are the "basic tools" of the semiconductor, communication, and new energy industries. At present, domestic high-end oscilloscopes have achieved a breakthrough in mass production at 90GHz, breaking the monopoly of overseas technology. The industry's gross profit margin exceeds 50%, and R&D investment accounts for over 25%, with strong technical barriers and profitability.

(2) Sensors and sensing chips: the "core heart" of instruments and meters

Companies such as Wanjie Electronics, Audi Way, Hanwei Technology, and others have flocked to the market, covering fields such as ultrasound, gas, and wireless sensing. Sensors are the core components of intelligent manufacturing, the Internet of Things, and automotive electronics, with a domestic substitution rate of only 35% and a broad market space. The automotive and industrial sensing sectors have benefited from the explosion of new energy and intelligent manufacturing, leading the industry in terms of growth rate.

(3) Precision testing and semiconductor equipment: a "must-have" for high-end manufacturing

Dazu CNC and Xinqi Microelectronics focus on PCB, semiconductor testing and lithography equipment, which are key links in the semiconductor industry chain. With the expansion of domestic semiconductor production capacity, the demand for domestically produced precision testing equipment has surged. Enterprises rely on technological breakthroughs and gradually enter core supply chains such as TSMC and SMIC, with strong growth certainty.

(4) Industrial Automation and Intelligent Instruments: AI Empowers New Growth

Eston and Haiqing Zhiyuan represent the direction of industry intelligence, integrating AI, IoT, and traditional instruments, upgrading from "perception tools" to "intelligent decision-making centers". The demand for industrial robots, intelligent monitoring systems, and fault prediction equipment continues to rise, becoming new growth engines in the industry.

Opportunities and Challenges: Cold Thoughts on the Industry under the Trend of Listing

(1) Core opportunities

Technological breakthrough acceleration: Hong Kong stock market fundraising will continue to invest in high-end research and development, promote breakthroughs in core chips, precision processes, and algorithm technologies, and accelerate the process of domestic substitution of high-end instruments.

Reshaping the global landscape: A+H enterprises rely on dual platforms to accelerate overseas factory construction, mergers and acquisitions, and channel layout, changing the pattern of "foreign capital leading the world" and increasing the global share of domestic instruments.

Industry concentration improvement: Capital is concentrated towards leading companies, promoting the clearance of small and medium-sized enterprises, shifting the industry from "decentralized competition" to "leading companies", and optimizing the industrial structure.

(2) Main challenges

High end competition intensifies: Foreign giants rely on their technological, ecological, and brand advantages to increase their counterattack in the high-end market, while domestic enterprises face the dual pressure of "technological catch-up+market competition".

Profit differentiation concerns: The industry presents a pattern of "top profit, tail pressure", with some companies experiencing a decline in net profit by 2025, and R&D and cost pressures continuing to erode profits.

Valuation fluctuations of Hong Kong stocks: Hong Kong stocks are greatly affected by global macroeconomic and exchange rate fluctuations. If the market weakens, it may lead to low valuations of enterprises, affecting financing effectiveness and refinancing plans.

Future outlook: A new journey of high-quality development in the industry empowered by capital

The wave of Hong Kong stock listings from 2025 to 2026 is an important turning point for the instrumentation industry, from "following the trend" to "running in parallel" and from domestic to global. In the next 3-5 years, the industry will present three major trends:

One is the comprehensive deepening of high-end substitution: driven by policies, capital, and technology, the localization rate of high-end instruments will continue to increase, and is expected to exceed 50% by 2030, with the dependence on imported core components dropping below 30%.

The second is the new pattern of global competition: "A+H" leading enterprises will become the main force in the global market, competing head-on with international giants such as Thermo Fisher Scientific and Thermo Fisher Scientific, and the global share of domestic instruments will increase from 15% to over 25%.

The third is the transformation towards intelligence and integration: AI, big data, and the Internet of Things are deeply integrated, and instruments are upgraded to an integrated "hardware+software+service" model. The industry has entered a new stage of high-quality development with "intelligent perception, intelligent decision-making, and intelligent operation and maintenance".

The wave of Hong Kong stock listings is not the end, but a new starting point for the domestic instrument and meter industry to break through. Under the empowerment of capital, a group of Chinese instrument and meter leaders with global competitiveness are accelerating their rise, which will not only rewrite the global industrial landscape, but also lay a solid core foundation for China's independent and controllable high-end manufacturing.